According to Article 4, Law on DI, “Deposit insurance means a guarantee to reimburse insured depositors up to a deposit insurance limit when an insured institution is incapable of paying deposits to depositors or goes bankrupt”.

Deposit insurance coverage limit in Vietnam over the years

The DI coverage limit is stipulated in Clause 1, Article 24, Law on DI “Insurance limit is the maximum deposit insurance amount to be paid by the deposit insurance organization for all insured deposits of a depositor at an insured institution when insurance payment duty arises”.

According to international practice, DI policies focus on protecting the interests of the majority of customers, who are small depositors with low income, have little access to information and unable to choose which bank to deposit money at. In Vietnam, the small customers account for about 75-80% in terms of number and their deposits account for only 10-15% of the total deposits at banks.

The DI coverage limit is determined in accordance with the socio-economic characteristics of each country; however, it generally depends on these basic factors: Gross domestic product (GDP) per capita; the ratio of insured depositors to total depositors; and the size of the DI fund.

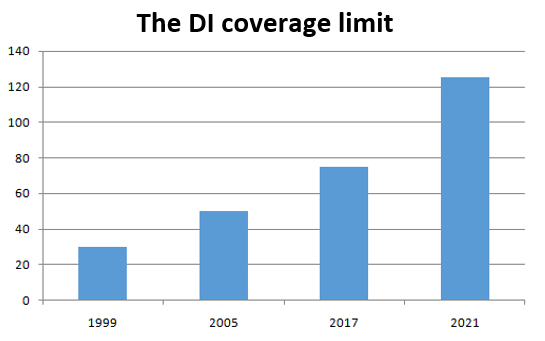

In Vietnam, the initial DI coverage limit (in 1999) was VND30 million per depositor per insured institution. This limit was considered appropriate with international practices at the time of application, which was equivalent to 5.5 times of the GDP per capita and about 80% of total depositors could be fully insured if the bank went bankrupt, while the DI coverage limit in the world was about 3-12 times of the GDP per capita.

In 2005, the DI coverage limit was adjusted to VND 50 million, about 3 times of GDP per capita and therefore about 81% of total depositors could be fully insured [1].

In 2017, the DI coverage limit was increased to VND 75 million, capable of fully protecting about 87,32% of total depositors [2], equivalent to 1.5 times GDP per capita in 2016.

The DI coverage limit

However, the fast pace of economic and consumer prices growth in the past 4 years have made this coverage limit no longer appropriate, since the income and average deposit amount of depositors have far exceeded the VND 75 million. When the insured institution is closed, goes bankrupt, and incurs DI payment obligation, depositors can only be paid the maximum amount of VND 75 million – 1.2 times of GDP per capital in Vietnam in 2020 – about 2,750 USD [3], which is quite small compared to international practice.

Enhancing depositor protection capacity

With the increasing growth rate of the consumer prices in recent years and GDP per capita expected to continue to go up in coming years, raising the DI coverage limit is not only a necessary but also urgent matter to help depositors feel more secure when depositing money into banking system, especially when the individual deposits are declining.

According to the data released by the State Bank of Vietnam (SBV), by the end of June 2021, while deposits of economic organizations into the banking system reached VND 5.11 million billion, an increase of 4.78% against the end of 2020, the individual deposits up by only 2.94% compared to the end of 2020, reached VND 5.29 million billion. This is the lowest growth rate of individual deposits compared to the same period in previous years (May 2012 up by nearly 16%, May 2013 up by 14.26%, and May 2014 to 2020 up by 9.49%, 8.31%, 11.04%, 9.39%, 7.5%, 6.84% and 4% respectively).

Experience shows that the higher the DI coverage limit, the more secure depositors will be when depositing money into the banking system. Specifically, since the Covid-19 pandemic shows unpredictable developments all around the world, many countries such as Armenia, Kenya, Bangladesh, Jamaica or the Philippines, etc. have also assessed, proposed to increase the DI coverage limit or already raised the DI coverage limit to expand the depositor protection capacity.

However, to which extend the DI coverage limit be adjusted depends on many factors, which was mentioned earlier, including the source of payment.

Many countries adjust the DI premium to ensure the payout capacity when the DI coverage limit is increased. However, raising the DI premium when the economy is heavily affected by the Covid-19 pandemic will increase the burden on credit institutions, affecting the operational efficiency of the banking system. On the other hand, beside preparing for payout fund, the DI agency need to maintain an appropriate amount to support the insured institutions, prevent the risk of insured institutions being closed or going bankrupt, and failures resolution.

In Vietnam, over 20 years of operation, from the initial VND 1,000 billion, the DIV has accumulated and invested the revenue from DI premium to increase the total assets to over VND 70,000 billion, in which the operational provision fund reached more than VND 64,000 billion. This is an important financial foundation for the DIV to accomplish the mission of protecting depositors through DI reimbursement with appropriate DI limit aligned with the international practices and standard, without increasing DI premiums.

The SBV has proposed to the Government to increase the DI coverage limit to VND 125 million per depositor per insured institution. This number nearly doubles the GDP per capita in 2020 and at this rate about 90.94% of total depositors will be fully insured. This DI coverage limit is more appropriate with international practices and should be approved by the Government in a timely manner to better protect the interests of the depositors.

Raising the DI coverage limit not only expands the depositor protection capacity, but also makes depositors feel more secure when depositing money into the banking system, contributing to the growth of capital mobilization in the context of declining individual deposits growth rate, spurring the development of the national economy.

Research and international cooperation department

References:

[1] https://vnexpress.net/ngan-hang-muon-tang-han-muc-bao-hiem-tien-gui-2683142.html

[2] https://www.pti.com.vn/-bao-hiem-tien-gui-bao-ve-duoc-87-32-so-luong-nguoi-gui-tien.htm

[3] https://nhandan.vn/nhan-dinh/vi-the-va-co-do-kinh-te-viet-nam-631311/