The Operational Reserve Fund is derived from the following sources: annual deposit insurance premiums; return on investment of temporarily idle capital after being deducted to cover the operational costs of the DIV as legally prescribed; unclaimed insurance pay-outs as legally prescribed; proceeds (if any) from liquidation of public institutions' assets; difference between the remaining annual income and expenditure after deduction for the Investment and Development Fund and the Bonus and Welfare Fund; and earnings from special loans provided to credit institutions under special control.

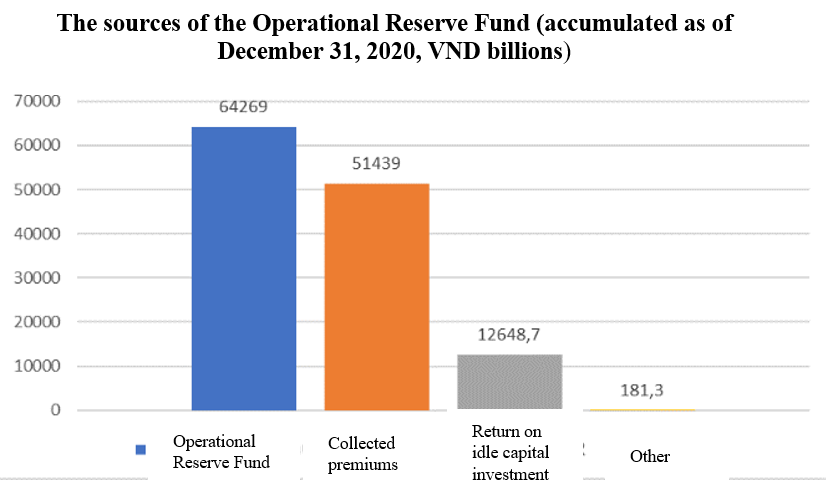

As of December 31, 2020, the DIV’s Operational Reserve Fund stood at 64,269 billion dongs, accounting for 91% of total capital (70,576 billion dongs), of which: collected DI premiums were 51,439 billion dongs; return on the investment of temporarily idle capital after being deducted by a sum into income was 12,648.7 billion dongs; revenue from other activities was 181.3 billion dongs (unaudited data).

Revenue from the DI premium collection and investment of temporarily idle capital accounted for 99.7% of the Operational Reserve Fund. This article assesses the two main sources forming the DIV’s Operational Reserve Fund.

Premium collection

Since its establishment, the DIV has applied an ex-ante funding mechanism and charged a flat rate of 0.15% of total eligible deposits at each insured institution. This has enabled the DIV to be financially ready to make payouts when necessary. However, a premium collection mechanism, especially when the Operational Reserve Fund is in short or a financial crisis breaks out, has not yet been available in Vietnam. This is one of capital mobilization channels for the DIV to execute the function of DI pay-out and ease the financial burden on the state budget.

Besides, the policy on DI premiums applied for financial institutions under special control has changed significantly. Specifically, since 2018 institutions under special control are exempted from payment of DI premiums in accordance with the amended Law No.14/2017/QH14 on Credit Institutions (CI). This exemption given to institutions under special control does not comply with the recommendations of the International Association of Deposit Insurers (IADI) as well as international practices, that is, weak financial institutions have to pay a higher premium rate than healthy financial institutions do according to the principle of risk-based premiums since they increase the risk of a breakdown in the system.

Return on investment of temporarily idle capital

Return on investment is the second main source of the Operational Reserve Fund of the DIV as well as other deposit insurers worldwide. According to the Law on DI, the portfolio of investment instruments and assets (ensuring the safety principle and risk provision as recommended by IADI), including: government bonds; long-term bonds of support credit institutions purchased according to the decisions of the State Bank of Vietnam (SBV); SBV bills; deposits at the SBV.

At present, the DIV is allowed to buy bonds, bills and deposit money at the SBV only to ensure high liquidity, low risk, but yield low return, which limits the DIV’s financial capacity growth and may induce many difficulties. In stable economic conditions, there is no mechanism for the DIV to make investments with higher profitability to accumulate more capital for the Reserve Fund, increase its financial capacity to reimburse depositors when necessary and ease the burden on the Government when the economy is in difficulty.

Before the enforcement of the Law on DI on January 1, 2013, return on the investment of idle capital had been totally included in the DIV's income. This had helped the DIV to be more proactive in accumulating capital for the Investment and Development Fund to increase the charter capital, and at the same time, this had facilitated the process of building annual financial plans.

Since 2014, the Law on DI and the guiding documents on the financial management regime for the DIV (the Circular No. 41/2014 / TT-BTC replaced by the Circular No. 312/2016 /TT-BTC dated November 26, 2016 and the Circular No. 20/2020/TT-BTC dated April 01, 2020 issued by the Ministry of Finance) have stipulated that the DIV deduct a part of earnings from investment of temporarily idle capital into the income at a rate annually regulated by the Ministry of Finance, the rest be transferred to the Operational Reserve Fund, so accumulated capital for the reserve fund is increasing. However, this has resulted in many administrative procedures, multiple times of making financial plans, and especially a low deduction rate for the Investment and Development Fund (the deduction rate is not more than 30% of the difference between revenue and expenditure). This also does not ensure sources for the Investment and Development Fund set for the purpose of increasing charter capital in the future, while according to the Government's orientation, only the Investment and Development Fund will be used to supplement state capital at state-owned enterprises according to the Circular No. 59/2018/TT-BTC dated July 16, 2018 amending and supplementing a number of articles of the Circular No. 219/2015/TT-BTC dated December31, 2015 and does not ensure the growth rate of the Operational Reserve Fund and Investment and Development Fund.

According to the Vietnam’s Accounting Law and Standard 14 –Other revenues and incomes, interests earned from financial investment such as earnings from investment in bonds and treasury bills are 100% accounted to income from financial activities. However, since the Law on DI came into effect, a small portion of earnings from the investment is included in income to cover operational costs, the rest added to the Operational Reserve Fund, and this does not follow the Accounting Law.

According to international practices, in some countries such as Taiwan, Canada, profits from investment are 100% recorded in income, not partly accounted to income and partly transferred to the Operational Reserve Fund as in Vietnam.

In general, as for the funding mechanism for the Operational Reserve Fund, basically the main sources of the Operational Reserve Fund such as DI premiums, return on investment ... follow the recommendations of IADI as well as international practices and the existing law has provided the mechanism, creating favorable conditions for the DIV to accumulate capital. However, there are still some shortcomings that need to be fixed in financing the Operational Reserve Fund, thereby increasing the sources and reserve mobilization for the Operational Reserve Fund.

Department of Internal Audit - DIV